Drought and Derecho Drive Crop Insurance Payments; Benefit to Land Values and Cash Rents

Photo by Daniel Acker/Getty Images

Farming has always been considered a high-risk business. It is essential for a farming business to navigate a multitude of decisions with a high level of business acumen to be profitable year-over-year. However, most of the risk associated with farming relates to events that are out of the operators control such as weather events and the direction of the commodity markets. The year 2020 gave us a reminder of those uncertainties as much of the crops in West Central Iowa suffered through a severe drought and a derecho windstorm that blew across the corn belt beginning in Nebraska and ending in Indiana. The windstorm affected approximately 750 miles of corn and soybean acres and the damage amount has varied among different sources, but the Risk Management Agency (RMA) estimates the total derecho crop damage to have cost over $6 Billion. Most farmland operators and owners quickly contacted their crop insurance agent or dug out their crop insurance file to check their policy and coverage levels purchased prior to the crop being planted. The reports of the derecho storm and drought damage began to dominate most conversations with the discussion including the nature of how crop insurance payments would affect the profitability of the farm sector. A high percentage of farmers and farm operators will have a crop insurance claim for the 2020 farm year and this article explores how the surge in crop insurance payments could offer support to balance sheets and subsequently boost cash rents and land prices into 2021.

The intent of crop insurance is to serve as a risk management tool available to farmers and ranchers to help protect against declines in crop yields and revenue by creating a safety net of farm income. Federal crop insurance was first authorized by Congress in the 1930s to assist the agricultural sector in recovering from the Great Depression and the Dust Bowl. In 1980, legislation was passed to encourage participation in the Federal Crop Insurance Program and to subsidize the products so they could be more affordable to producers. This marked the introduction of a public-private partnership between the U.S. government and private insurance companies where the government would contribute financially to assist in lowering the overall cost of crop insurance. Crop insurance has become a staple to most all operations and in 2019, more than 90% of the nation’s insurable farmland, or roughly 370 million acres, were enrolled in the Federal Crop Insurance Program. There are several different crop insurance products that are available at various coverage levels with options for additional endorsements. The level or type of crop insurance purchased is usually a reflection of the risk profile of the operator or the revenue protection required by a lending institution to cover or service a loan payment. The two primary crop insurance types are hail insurance and multi-peril insurance. Multi-peril insurance provides coverage options to farmers that combine yield protection and price protection against potential loss in revenue due to low yields or changes in the market commodity price.

To demonstrate how crop insurance works and the potential complexity of the various products, an example will be utilized of a 160-acre farm owned and operated by a fictional farmer Bob Bushels. Bob purchases a multi-peril crop insurance policy and decides on an 85% coverage level for corn crop. Bob has an Approved Production History (APH) of 200 bushels per acre on his farm and the insurance policy will guarantee 85% of the APH of 200 bushels per acre, which is 170 bushels per acre. The premium for this policy is $33 per acre and the revenue guarantee for this farm will be determined by taking the “spring price” (the average commodity price during the month of February) times the guaranteed bushels. Assuming the spring price is $4 per bushel, Bob would take the commodity price of $4 times the guaranteed 170 bushels and would have a total of $680 of coverage per acre. Simply said, Bob would have a guaranteed revenue amount of $680 per acre under this policy.

To further the example, Bob would like to purchase additional insurance by adding a hail insurance policy. This policy would be in addition to the multi-peril policy and adds additional revenue protection in the event of crop damage due to hailstorm or wind damage. Hail insurance can vary in coverage and expense, but Bob makes the decision to purchase a policy that will cover a maximum of $500 per acre with an added “Extra Harvest Expense” endorsement, which will pay an additional $40 per acre if wind damage occurs to more than 10% of the crop. This policy will cost an additional premium of $12 per acre. If a hailstorm takes place and an insurance claim is made, Bob will essentially receive $5 for every 1% of damage up to a total payment of $500. If there would be a total crop loss because of a hailstorm, Bob would receive both his multi-peril Federal Crop guarantee of $680 per acre and the hail insurance policy of $500 per acre, for a total of $1,180 per acre.

A farmer or producer can also increase their revenue coverage on a multi-peril insurance policy. Bob Bushels opts to add an additional 10% of revenue protection in addition to the original 85% policy he purchased. The additional 10% that Bob purchases would adjust his bushel guarantee from 170 bushels per acre to 190 bushels per acre, or an increased revenue guarantee from $680 per acre to $760 per acre. This additional $80 of revenue coverage that Bob purchases is more costly than his original 85% policy because of a higher probability of collecting a payment at the elevated price and yield levels; therefore, the extra 10% of coverage costs an additional $40 per acre. The total insurance Bob Bushels has purchased in this example would include a guaranteed revenue protection of $760 per acre (computed as 190 bushels per acre times the $4 per bushel “spring price”) and a hail/wind insurance policy that would contribute up to $500 per acre from a hailstorm event. The total investment Bob would make for this insurance plan would consist of $85 per acre of insurance premiums ($33 plus $12 plus $40). Margins in farming have been thin in recent years and committing $85 per acre for crop insurance has been a challenge. Utilizing crop insurance should be considered a core expense in a farming operation but farm operations should consult with a professional to determine the optimal amount of coverage that aligns with the producer’s risk tolerance. The revenue guarantee protection provided by a crop insurance policy should cover a desired level of farm expenses to prevent potential financial hardship created by weather elements or fluctuations in commodity prices.

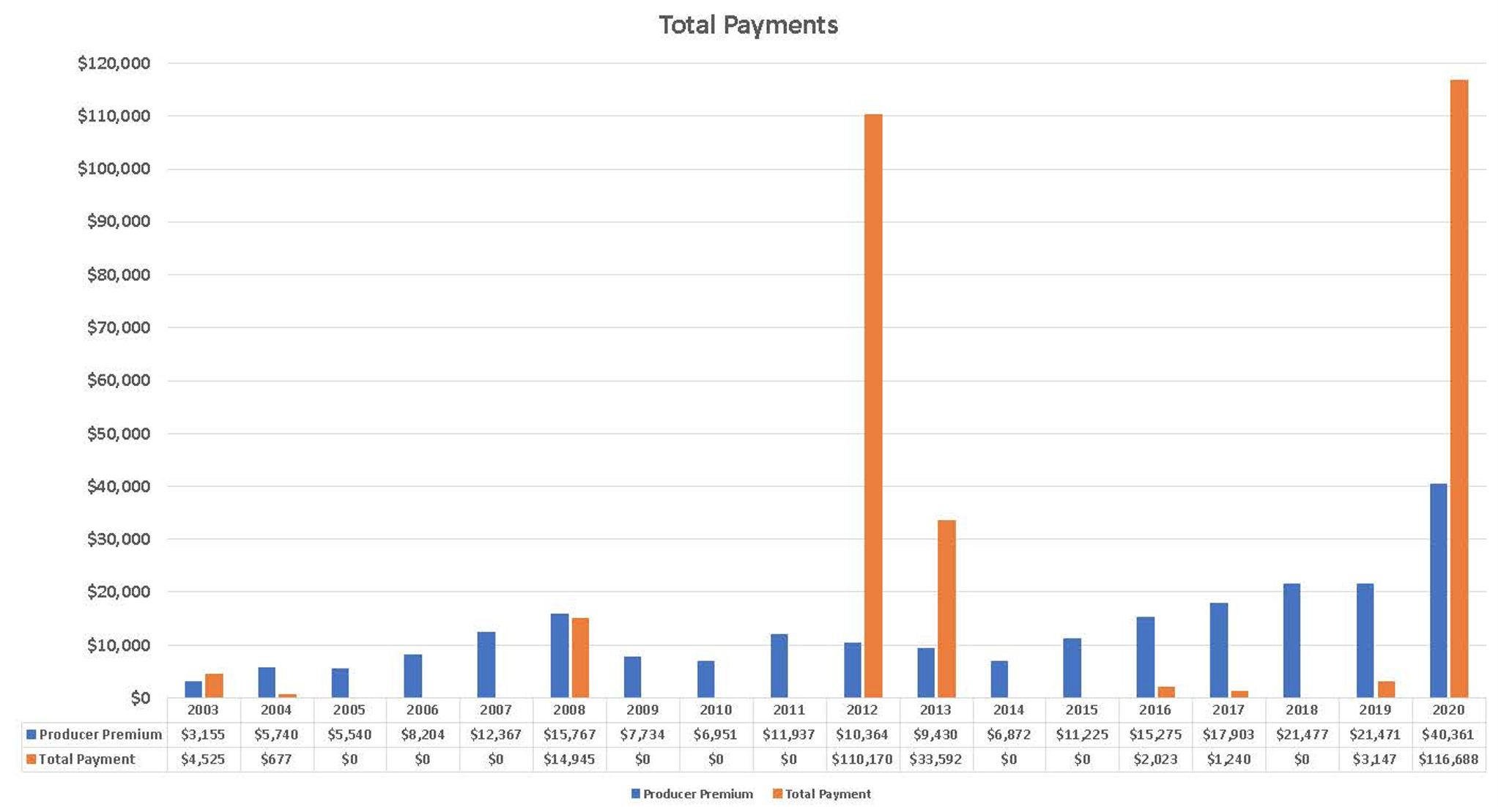

The weather events of 2020 have created potential opportunities for farm operations with above-average crop insurance payments. Crop insurance specialist Luke Wendl with Agri Serv, Inc. in Panora, Iowa, provided historical data for a farming operation comparing crop insurance premiums paid versus the crop insurance payment received for each year from 2003 through 2020. The farming operation consisted of just over 1,500 acres in Central and West Central Iowa (Dallas County and Guthrie County) and had a variety of farm lease arrangements including farmland that he owned and farmed himself, cash rental agreements, and crop share agreements. The percentage of crop insurance premiums and crop insurance payments adjusted depending on the type of farm lease arrangement.

The chart below illustrates the annual amount the farming operation paid for crop insurance compared to the total amount received for each year. The blue bars represent the total annual premium paid and the orange bar corresponds with the total annual payment received for that given year. For 14 of the 18 years, the crop insurance premium paid by the operator outpaced the crop insurance payment received or payment was not received at all. However, four out of the 18 years (2003, 2012, 2013, and 2020) triggered crop insurance payments far greater than the crop insurance premiums paid. The extreme weather events in 2012, 2013, and 2020 created windfall payments compared to the insurance premium paid with the 2012 indemnity payment paying 10X the premium, 3.5X the premium in 2013, and just under 3X the premium in 2020! (*Note the crop insurance payment to be received in 2020 is estimated, as claims have not been turned in and the fall price used to determine payment levels has not been established at the time this article was written.) These types of returns would be considered an anomaly and should not be expected on an annual basis. Looking at the graph, the total premium payments compared to the indemnity payment received in 2003 through 2019 shows a $21,093 loss to the farm operator, however, when the anticipated crop insurance payment for 2020 is added to the total indemnity payments received, this adjusts to a gain of $55,234.

An argument can be made that a crop insurance payment received is essentially offsetting grain sales that would have otherwise taken place had the yield or price not been affected and prompted a crop insurance payment. Still, the effect of an acute weather or negative price event likely lowers yield and supply prospects, which in turn should increase overall commodity prices.

How will the 2020 crop insurance payments affect the outlook for land prices and cash rents? Crop insurance distributions and the historical peak of the land market have a high correlation for the years 2012 and 2013, where the average price of an acre of farmland in 2012 was $8,296 and $8,716 in 2013. Farm operations that purchased ample crop insurance coverage for the 2020 farm year will likely see improved income on their balance sheets. Furthermore, improved balance sheets should support land prices and cash rents for the 2021 farm year. Other drivers of the farmland market are interest rates, increased commodity prices, and a flight to safety as the stock market continues its volatile streak while raring from the coronavirus pandemic and the political sparring in Washington. The next six months will offer answers to these questions and should substantiate the notion of how crop insurance might affect cash rents and land prices.

Peoples Company land managers employ crop insurance as a tool to limit downside risk for custom farming operations and crop share farm lease arrangements. Engaging professionals such as Luke Wendl at Agri Serv, LLC allows Peoples Company to provide a better service to farm and land management clients. If you, a colleague, or a client of yours is interested in learning more about the opportunities or viability of a custom farming operation or crop share farm lease, please don’t hesitate to contact Peoples Company and speak to Matt Adams or one of our land managers, Kyle Walker.

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.