Land Prices: Trending Up

Interest rates have been a highly correlated determinant of farmland values from the inception of farmland financing, and especially since the early 1900s when the Federal Land Bank and subsequent institutions increased the sophistication of the business of extending credit to those looking to add farmland to their operations. The relationship between interest rates, or the cost of money, and farmland is inverse in that an increase in interest rates should pressure farmland prices lower, and alternatively, a decrease in interest rates should support higher land values. The current interest rate environment is much more favorable than that of a year ago and should cause the farmland market to trend higher.

Throughout 2018 and 2019, the government began increasing the Federal Funds rate to curb potential inflation and maintain their target growth rate of around 2%, effectively increasing U.S. treasury rates. That effort was interrupted in March 2020 when the government responded to the coronavirus pandemic by lowering interest rates to combat the negative effects of coronavirus by maintaining access to capital for individuals and businesses. A reoccurring thought and subsequent conversation I have had with myself and clients are if lower interest rates have increased farmland prices or are current interest rates “baked into” or reflected in today’s farmland prices? I would argue that interest rates are not fully reflected in current farmland prices. Farmland has always been described as having unique, individual characteristics and although technology has made great strides in commoditizing the farmland market, the farmland market doesn’t adjust to new information or economic factors as quickly as the stock market, where the price of a stock adjusts instantaneously to any relevant news or information that becomes available. The farmland market reacts slower and in longer-term trends than immediate price adjustment. Market factors that assist the slower price response are farm leases and cash rents, which are paid once per year, the volume of farmland on the open market, which has been very limited, and probably more than anything the farmland market has a tendency to be much more emotional and reliant upon the location of the farmland compared to other investments.

To illustrate how powerful interest rates can be in the value of farmland specifically, below are two examples of realistic farm financing in today’s world. Assume a land buyer wants to purchase 133 acres at $7,500 per acre. The bank or lending institution will lend them 70% of the purchase price over a 20-year period at a fixed interest rate for five years. One example uses an annual interest rate of 5.5% and the other applies an interest rate of 3.55%. It might be hard to believe, but towards the end of 2019 the cost of borrowing was closer to 5.5%, and less than six months later interest rates had adjusted to 3.55%.

Fall of 2019

Purchase Price: $997,500 (133 Ac @ $7,500 / Ac)

Down Payment: $299,250 (30%)

Amount of Loan: $698,250

Interest Rate: 5.5% Fixed for 5 Years

Amortization: 20 Years

Annual Payment: $58,430

Fall of 2020

Purchase Price: $997,500 (133 Ac. @ $7,500 / Ac)

Down Payment: $299,250 (30%)

Amount of Loan: $698,250

Interest Rate: 3.55% Fixed for 5 Years

Amortization: 20 Years

Annual Payment: $49,350

You can see in the example above that the difference in the annual payment is around $9,000 per year. The simplest way of looking at this is that a borrower that had purchased farmland in the fall of 2019 could refinance their current loan from 5.5% to 3.55% and save approximately $9,000 per year in interest payments. Let us now look at how the purchase price for the same farmland property would adjust if the annual payment stayed the same under both the 5.5% and the 3.55% interest rate examples. Assume that the borrower initially purchased the farm with the understanding that their payment would be around $440 per acre (annual payment of $58,430 divided by 133 Acres) at a 5.5% interest rate. If that borrower wanted to maintain their $440 per acre payment, that same borrower could afford to pay an additional $183,575 ($1,380 per acre!) for the same property at a 3.55% interest rate.

Purchase Price: $997,500 (133 Ac @ $7,500 / Ac)

Amount of Loan: $698,250

Interest Rate: 5.5% Fixed for 5 Years

Amortization: 20 Years

Annual Payment: $58,430

Purchase Price: $1,181,075 (133 Ac. @ $8,880 / Ac)

Amount of Loan: $826,750

Interest Rate: 3.55% Fixed for 5 Years

Amortization: 20 Years

Annual Payment: $58,430

With the interest rate alone as our guide, the same 133-acre farm could sell for $8,880 per acre under a 3.55% interest rate compared to $7,500 per acre under a 5.5% interest rate. This is an oversimplified example that does not take into consideration what buyers would actually justify paying based upon an appraisal for a sales price; however, it does give insight to the trend that should follow an increase or decrease in interest rates.

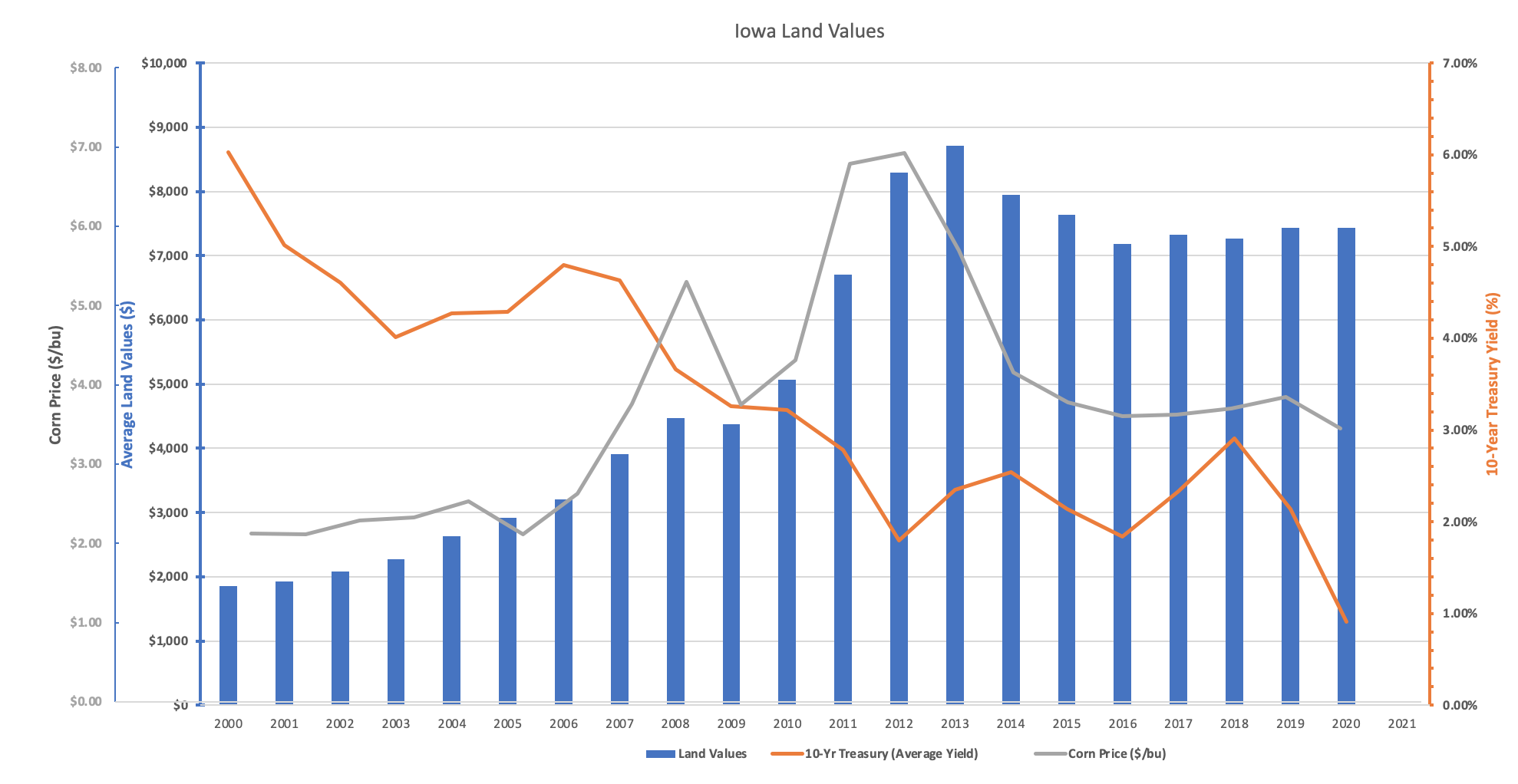

Other than interest rates, considerations that affect farmland values are cash rents and commodity prices. The chart below demonstrates the relationship between the average price of land, the average corn price, and the average Federal Funds rate for the range of years between 2000–2020. The two primary factors for the value of farmland are interest rates and commodity prices. This chart shows the trend of increasing farmland values (blue bar) while interest rates have fallen (orange line). Also, note in the years 2012–2014, it was a perfect storm for land values with low interest rates and elevated commodity prices (gray line). The most recent drop in interest rates are offering a beneficial borrowing situation for not only new farmland purchases, but the refinancing of a current farmland holding would benefit tremendously with generally less interest being paid and more of the annual payment being applied to the principal component of the loan.

There are several elements that determine the market value of farmland, however, barring any substantial adjustments to the overall environment (i.e. commodity price adjustments, changes in government guidelines, market volatility), the farmland market should benefit from lower interest rates or at least help to sustain current levels. The present economy promotes maintaining a lower interest rate environment to stimulate investment and encourage access to capital until elevated inflation warrants an increase in the target rates. Until then, our views are that farmland values will trend higher from the benefit of the lower cost of borrowing.

Peoples Company prides ourselves as being both consultants and salespeople in that we want to help Buyers and Sellers make decisions based on current information and attempt to offer future insights into what might affect the land market. Matt Adams with Peoples Company would welcome an opportunity to visit with you regarding the land market and what seems to be driving current prices.

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.