The Cost Approach: What Investment Tells Us About Land Value

Originally published by Iowa State University. Co-authored by Rabail Chandio and Emily Oberbroeckling.

This article is the second in a three-part series examining the primary methods used to appraise farmland in Iowa and across the Midwest. The first article explored the income approach and how earning power, capitalization rates, and discounting future cash flows help explain farmland values.

While the income approach answers the question, "What can this land earn?" the cost approach asks something different: "What would it cost to recreate this property today?" For improved agricultural properties (see Note 1), particularly those with grain storage, livestock facilities, machine sheds, or rural commercial buildings, the cost approach provides a practical means of separating land value from improvement value and of measuring how construction costs and depreciation influence overall market value. In periods of rising construction costs, evolving building standards, and specialized agricultural infrastructure, understanding the cost approach helps producers, lenders, and landowners interpret how investments in buildings and site improvements contribute to property value.

The Cost Approach is based on the premise that a typical buyer will not pay more for a property than the cost to acquire comparable land and construct improvements that provide the same utility. This approach is applicable to highly improved agricultural, rural, and commercial properties because many buildings, such as barns, grain storage, livestock facilities, and machine sheds, are specialized for a specific use and are not often sold.

Step 1: Estimate bare land value

The first step is to estimate the land's value as if it were vacant and available for its highest and best use (see Note 2). For agricultural and rural properties, this may include crop production (tillable land), livestock (pasture) use, rural building-site use, or a combination of these uses.

Land value is typically based on comparable land sales and considers factors such as:

Location and access,

Soil quality and productivity,

Utilities and water availability,

Zoning and land-use regulations.

This step answers the question: What is the land worth by itself, without any buildings on it? Appraisers may rely more heavily on the income or sales comparison approaches when estimating the value of land independent of any improvements.

Step 2: Estimate "Cost New" of improvements (RCN)

Next, the cost to build the existing improvements is estimated as of the effective date of the appraisal. This cost is referred to as RCN, which can mean either:

Replacement Cost New (RCN): The cost to build a new improvement that serves the same purpose and function as the existing one, using modern materials and construction standards. For example, the cost of replacing an older wooden machine shed with a modern steel building of similar size and utility.

Reproduction Cost New (RCN): The cost to build an exact copy of the existing improvement, using the same design, materials, and construction methods. For example, the cost of rebuilding a historic barn using the same wood framing, layout, and materials.

For most agricultural and commercial appraisals, replacement cost new is used because buyers are concerned with utility and efficiency rather than exact duplication.

Cost estimates are developed using a combination of nationally recognized cost services and market-based data. Appraisers commonly rely on published construction cost manuals such as Marshall & Swift and the National Construction Estimator, which provide benchmark costs for various building types, quality levels, and regional cost modifiers. These sources are frequently updated to reflect changes in material and labor costs.

Because agricultural buildings often vary in design, materials, and specialized equipment (such as grain-handling systems, ventilation, or livestock-confinement components), national data are typically supplemented with local contractor quotes, supplier pricing, and cost information from recent agricultural construction projects in the market area.

The objective is to estimate, as of the appraisal's effective date, the full cost to construct an improvement with equivalent utility and functionality. This total cost reflects all components necessary to place the structure into service, including direct construction costs (materials and labor), installation of specialized equipment, contractor overhead and profit, and an entrepreneurial incentive representing the return required to undertake the project.

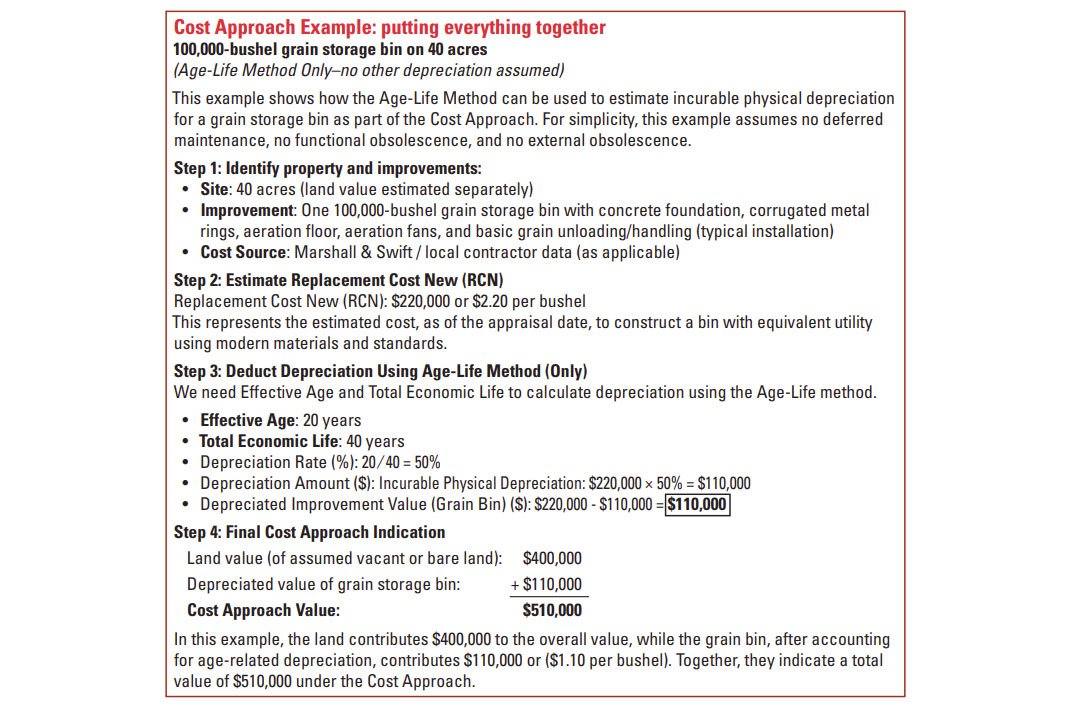

Step 3: Deduct depreciation (loss in value)

After estimating the cost new, depreciation is deducted to reflect the fact that most buildings are not new. Depreciation is the loss in value from any cause and is analyzed using the breakdown method, which examines each type of depreciation separately.

Breakdown method of depreciation

Physical deterioration is wear and tear from age, use, and exposure to weather. It can be further classified as curable or incurable which will determine its subsequent measurement.

Deferred Maintenance (Curable Physical Deterioration): These are repairs that are reasonable and cost-effective to fix. These are items a typical buyer would expect to repair after purchase. Examples include:

Fixing or replacing a worn roof on a barn,

Repairing damaged doors on a machine shed,

Electrical or plumbing repairs in a livestock facility,

Concrete repairs in shop or feeding areas.

Deferred maintenance is handled by estimating the cost to cure (the cost to fix the problem) and deducting that amount directly from the cost new.

Incurable Physical Deterioration: This is loss in value that cannot be reasonably fixed. It usually occurs because the building is older and part of its useful life has already been used up. Examples include:

An older livestock barn that still functions but is well past its prime,

Aging grain storage that remains usable but has limited remaining life.

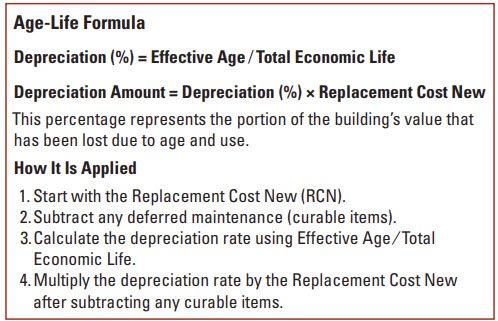

This type of depreciation is commonly measured using the Age-Life Method.

The Age-Life Method estimates incurable physical depreciation by comparing a building’s effective age to its total economic life. In simple terms, it measures how much of the building’s useful life has already been used up.

Effective Age reflects how old the building appears to be based on its condition and level of maintenance, rather than its chronological age. For example, a well-maintained 30-year-old machine shed may have an effective age of only 20 years if it has been properly maintained and updated.

Total Economic Life is the total number of years the building is expected to contribute value in the marketplace. This is not just how long the structure can physically stand, but how long it remains economically useful. For instance, a machine shed may have a 50-year economic life, while grain storage facilities may have a shorter economic life due to technological changes or shifting production practices.

Functional obsolescence is a loss of value resulting from outdated design, layout, or capacity limitations, even when a building is in good physical condition. In agricultural properties, this may include things like:

low ceiling heights that cannot accommodate modern equipment,

livestock facilities that are inefficient compared to current production standards, or

older farm shops with limited electrical capacity.

Functional obsolescence is curable if the issue can be corrected at an economically justified cost; otherwise, it is incurable if the cost to fix the problem exceeds the value it would add to the property.

External (economic) obsolescence is a loss in value caused by factors outside the property and beyond the owner’s control. In agriculture, this may stem from factors like:

changes in commodity markets,

new regulatory or environmental restrictions, or

declining demand for certain types of agricultural buildings in a local area.

Because these influences originate externally, they typically cannot be corrected by improving the property itself and are therefore considered incurable. When present, external obsolescence is measured through analysis of market data and comparable sales.

Step 4: Final cost approach value

After all depreciation is deducted, the remaining value of the improvements is added to the land value. This produces the value indicated by the Cost Approach. The Cost Approach is given appropriate weight in the final value conclusion of the appraisal report reconciliation. The cost approach is particularly applicable to the analysis of improved agricultural, rural, and commercial properties with specialized improvements that are not frequently sold.

End Notes:

Note 1: In appraisal terminology, improvements refer to any man-made additions to the land. This includes buildings such as grain bins, and other constructed features like fencing. An improved agricultural property is farmland that includes these types of structures or site developments, as opposed to bare cropland or pasture without buildings. Agricultural and rural improvements may include:

Grain storage facilities (bins, dryers, handling systems)

Livestock facilities (dairy facilities, cattle barns, loafing sheds, swine finishing or confinement buildings)

Machine sheds and farm shops

Specialty agricultural storage (vegetable/ fruit warehouse) or rural commercial buildings

Feed mills, greenhouses, etc.

Site improvements such as fencing, concrete, utilities, and driveways

Note 2: Highest and best use refers to the reasonably probable and legal use of a property that is physically possible, financially feasible, and results in the greatest value. For agricultural land, this may include crop production, livestock use, rural residential development, or rural commercial use, depending on market conditions, zoning, access, and location.

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.