What's Driving Grain Markets?

What began as a rising tide in post-Derecho, 2020 turned into the perfect storm of high demand and an uncertain supply in 2021. So far, in 2022, the grain markets continue to ride that momentum. China bought record amounts of corn in 2021 and pushed grain markets across the board to highs not seen since 2012. That, combined with very little carryover from the 2020 crop and widespread drought in the Northern Plains, sent end-users scrambling to fill their grain bins. Ultimately, the drought didn’t have the impact that was expected. In fact, 2021’s corn and soybean crops turned out to be the largest in history.

The trend has been upward for both corn and soybeans this year but under a different set of circumstances. After spending most of the winter largely absent from the U.S. grain markets, China has just recently become an active buyer again. Domestic usage has been the primary driver of demand in recent months. Profit margins for ethanol have been strong, and ethanol plants have been running at full capacity. Soybean prices have benefited from the three-month-long bullish run in oil prices and strong demand for bean meal as livestock feed. Hot, dry weather in Brazil and Argentina has also been a factor. Both countries are currently harvesting a smaller than anticipated soybean crop.

The conflict between Russia and Ukraine has created anxiety across the markets in general but could have a particularly strong impact on the grain markets. Russia and Ukraine account for roughly one-third of the world’s wheat exports and nearly one-fifth of the world’s corn exports. Throughout Ukraine, ports and other infrastructure have been closed or damaged, and international grain traders like ADM and Bunge have suspended operations. Millions of bushels of Ukraine’s 2021 corn and wheat crops are essentially frozen in place. Ukrainian farmers would normally start planting the 2022 corn crop in the next couple weeks, but now that is in jeopardy. Banks are closed, and the ability to secure financing is nonexistent. Financing aside, shortages in fuel, seed, fertilizer and machinery operators are all but guaranteed. With two years’ worth of production at stake, this could alter the world grain supply into 2023 and beyond.

The ripple effect from this conflict will extend around the globe. Major grain importing countries like China and Egypt rely on Ukraine as a source of corn and wheat. China, for example, typically buys more corn from Ukraine than it does from the U.S. Unless conditions change soon, importers will have to start looking for alternatives to secure the grain their countries need. The U.S. is well-positioned to fill the void as the only other country in the world with a meaningful amount of corn readily available for export.

Domestically, the outlook is much more positive. Corn and soybean producers are coming off a great year in 2021. Input costs have increased dramatically, but farmers have still had ample opportunity to contract their 2022 crop for a profit. Dry weather could be a threat as the same La Nina weather pattern that influenced the 2021 growing season is still present going into the 2022 growing season. While no two La Nina patterns are the same, it’s likely that there will be some similarities. On top of that, there are all of the other day-to-day challenges that go along with producing a crop. The variables at play are complex, and uncertainty is high, but at least for now, it’s hard to make much of a case for lower grain prices.

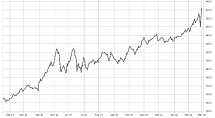

December Corn Futures 01/15/2021 –03/01/2022

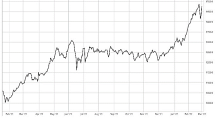

November Soybean Futures 01/15/2021 –03/01/2022

To learn more about managing your land around the changing grain markets in your area, contact Peoples Company Land Management at landmanagement@peoplescompany.com or visit our website www.PeoplesCompany.com

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.