Midwest Region

Regional Offices

Peoples Company - Bloomington

Midwest

Peoples Company - Cascade

Midwest

Peoples Company - Champaign

Midwest

Peoples Company - Cumming

Midwest

Peoples Company - DeWitt

Midwest

Peoples Company - Fremont

Midwest

Peoples Company - Independence

Midwest

Peoples Company - Indianola

Midwest

Peoples Company - Kasson

Midwest

Peoples Company - Kearney

Midwest

Peoples Company - Lincoln

Midwest

Peoples Company - Norfolk

Midwest

Peoples Company - Omaha

Midwest

Peoples Company - Oswego

Midwest

Peoples Company - Plainfield

Midwest

Peoples Company - Wapakoneta

Midwest

Peoples Company - Wayne

Midwest

Regional Listings

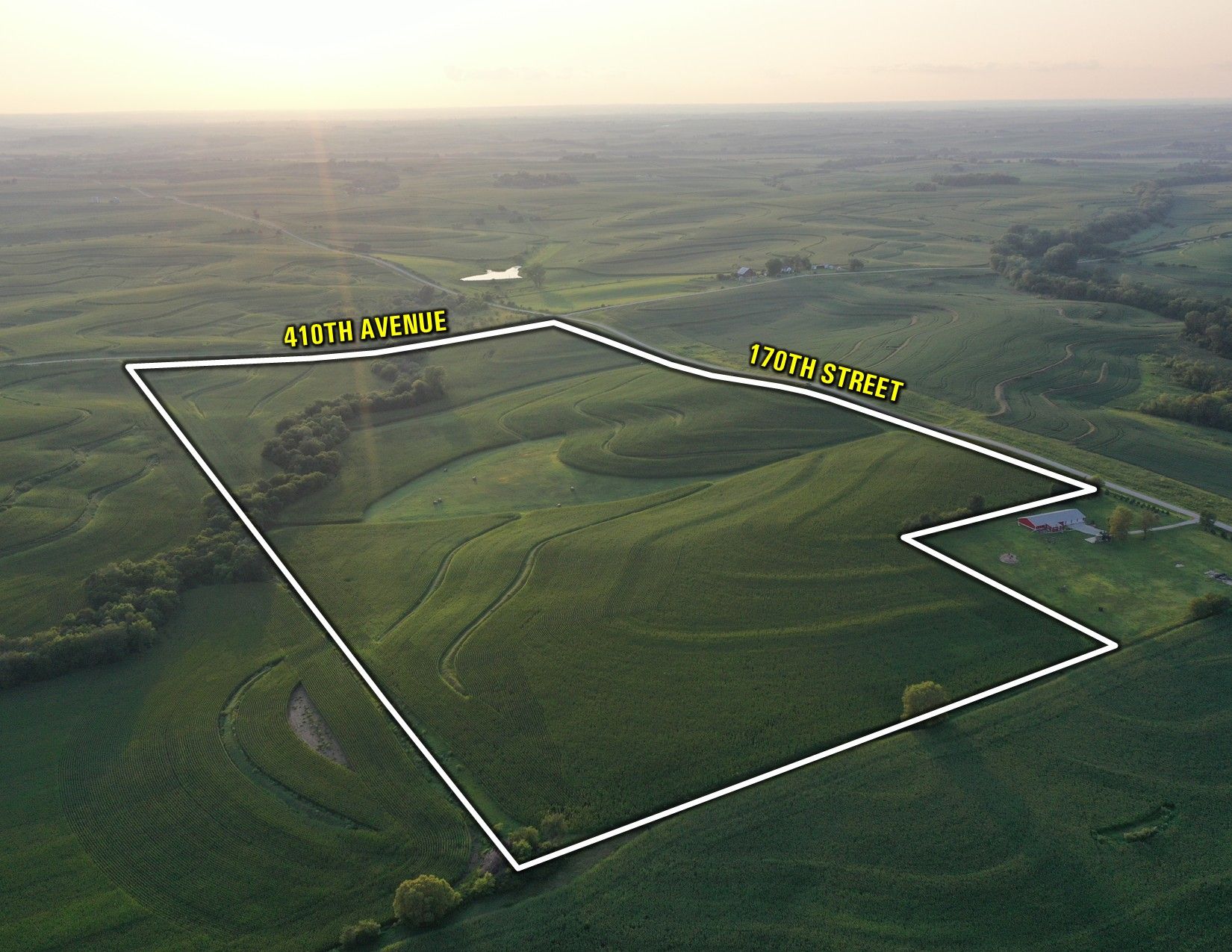

Fremont County, IA

170th Street & 410th Avenue

Shenandoah, IA 51601

Fremont County, Iowa Farmland Opportunity – Peoples Company is pleased to present 75.25 acres m/l located just north of Shenandoah, Iowa, along 170th Street and 410th Avenue. Situated just over a ha...

ACRES M/L

LISTING

Lucas County, IA

235th Trail

Chariton, IA 50049

Peoples Company is pleased to present 79.01 acres m/l located in Section 8 of English Township in Lucas County, Iowa. Offering 66.05 FSA cropland acres, this highly manageable tract presents an outsta...

ACRES M/L

LISTING

Fayette County, IA

247th Street

Waucoma, IA 52171

Fayette County, Iowa Farmland Available – Peoples Company is pleased to present 333.63 contiguous acres of Fayette County, Iowa farmland for sale, located directly adjacent to Alpha, Iowa. Large tra...

ACRES M/L

LISTING

.jpg)

Dallas County, IA

205th Street

Dallas Center, IA 50063

Upcoming Dallas County, Iowa Farmland Auction - Mark your calendars for Thursday, October 8th, 2026, at 10:00 AM! Peoples Company is pleased to be representing the Shirley Morgan Family Trust in the s...

ACRES M/L

AUCTION DATE

LISTING

Indianola, IA

804 E Ashland Ave

Indianola, IA 50125

Extensively remodeled 4-bedroom, 1¾-bath, 2-story home offering the efficiency and peace of mind of modern construction with the character of a classic home. Nearly every aspect of this property has ...

ACRES M/L

LISTING

Johnson County, IA

5371 Lower West Branch Rd Se

West Branch, IA 52358

Peoples Company is pleased to present a rare opportunity to acquire 66.10 acres m/l in highly sought-after Johnson County, Iowa. Ideally located just 3 miles from the Iowa City city limits, 7.5 miles ...

ACRES M/L

LISTING

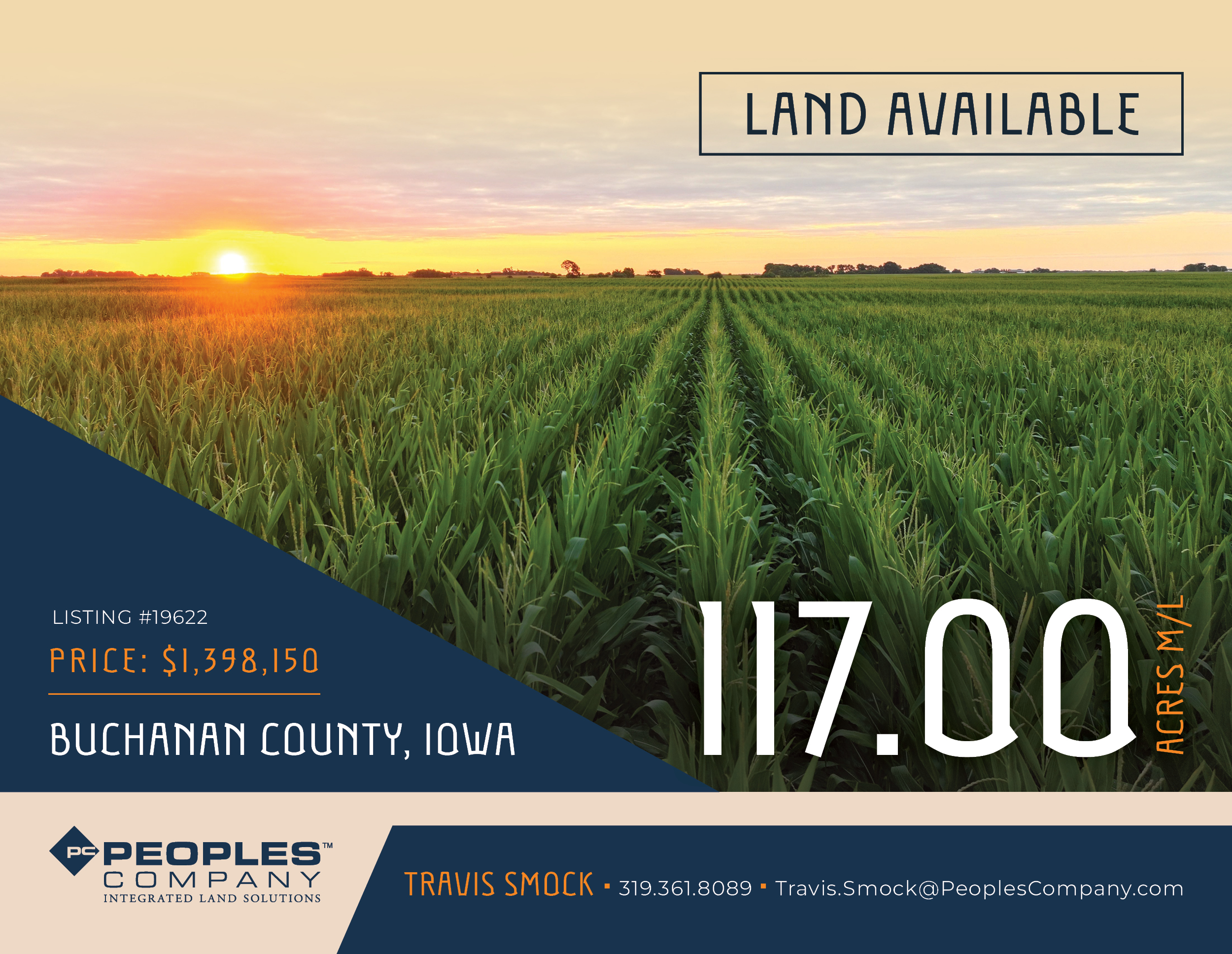

Buchanan County, IA

Dillon Avenue

Fairbank, IA 50629

Offering 117 acres m/l of high‑quality Buchanan County farmland located less than one mile from the Fairbank, Iowa POET ethanol plant. This premier eastern Iowa farm includes 106.75 tillable acres m...

ACRES M/L

$11,950 / ACRE

LISTING

Boone County, IA

105th Street/F Avenue & County Highway E26

Pilot Mound & Ogden, IA 50223

Boone County, Iowa Online Only Auction - Mark your calendars for Friday, September 25th! Peoples Company is pleased to offer two high-quality farmland tracts totaling 160 acres, located less than two ...

ACRES M/L

AUCTION DATE

LISTING

.jpg)

Greene County, IA

Terrace Avenue & 318th Street

Rippey, IA 50235

Greene County, Iowa Farmland Available! Peoples Company is pleased to present 168.07 acres m/l of Greene County, Iowa farmland located just northwest of Perry, Iowa, in the southeast corner of the cou...

ACRES M/L

LISTING

.jpg)

Greene County, IA

270th Street & C Avenue

Scranton, IA 51462

Productive Greene County, Iowa Farmland Available! Peoples Company is pleased to present 229.69 acres m/l of high-quality Greene County farmland owned by the Beverly L. Hoyt Revocable Trust located so...

ACRES M/L

LISTING