EIA Short-Term Energy Outlook | Oil, Gas & Power Market Updates

The newest EIA Short-Term Energy Outlook (STEO) highlights shifting trends across oil, natural gas, and power markets, with updates that carry real implications for budgets and strategy. Energy decision-makers need quick clarity on what changed, why it changed, and what it means for planning in the months ahead.

Key Takeaways

Oil markets are stable but remain tied to OPEC+ decisions and global demand risks.

Natural gas faces competing forces: strong supply and storage vs. rising LNG exports.

Power generation continues its transition, with renewables gaining ground while coal falls further behind.

Introduction – Why the STEO Matters Right Now

The Short-Term Energy Outlook is one of the most-watched energy forecasts in the world, released monthly by the U.S. Energy Information Administration. It offers two-year projections for production, consumption, and prices across fuels. For energy buyers and utilities, the STEO is a pulse check on where markets may be heading and how to plan accordingly.

This month’s report includes revisions shaped by shifting production levels, ongoing global policy decisions, and updated weather expectations. While forecasts can never predict every outcome, they provide a baseline that helps businesses hedge costs, utilities shape supply plans, and policymakers anticipate challenges.

Key Numbers Snapshot

This month’s highlights include:

Brent crude oil: Revised upward slightly due to tighter inventories and strong Asian demand.

WTI crude oil: Closely follows Brent, with only modest changes.

Henry Hub natural gas: Adjusted downward as robust production and above-average storage reduce price pressure.

U.S. crude oil production: Expected to reach record levels, with efficiency gains offsetting fewer rigs.

Electricity generation: Renewables gain more share, coal declines, and natural gas remains steady.

These revisions underscore how fluid energy markets remain, and why monitoring each monthly STEO update is essential.

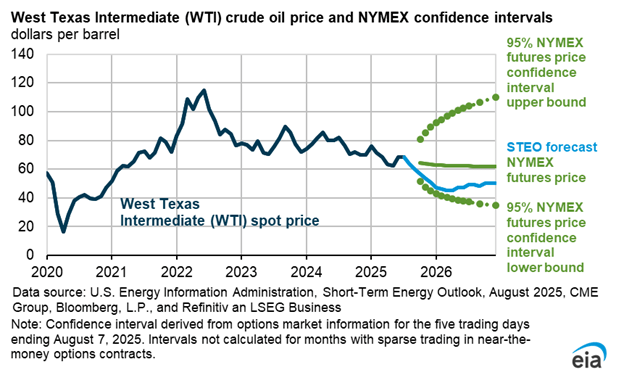

Oil Outlook – Prices, Supply, and Demand

Price Forecasts and Market Drivers

Price Forecasts and Market Drivers

EIA’s slight upward adjustment to Brent reflects tighter inventory balances, paired with resilient Asian demand. Oil prices remain influenced by OPEC+ production agreements, which have kept supply intentionally tight in recent months.

That said, risks remain on both sides. Slower global growth or rising interest rates could dampen demand, while geopolitical conflicts and shipping disruptions could quickly push prices higher. For businesses exposed to fuel costs, this combination of modest forecasts with heavy upside risks suggests caution when setting long-term budgets.

U.S. Production and Exports

Domestic production continues to surprise to the upside, with record-setting output expected this year. Shale operators, especially in the Permian Basin, are achieving more output per rig, offsetting a smaller rig count.

Exports of crude and refined products remain a critical part of the U.S. energy picture. As overseas refiners and buyers look for stable supply, U.S. oil has become a balancing force. This trend benefits global stability but can also amplify domestic price sensitivity to global events.

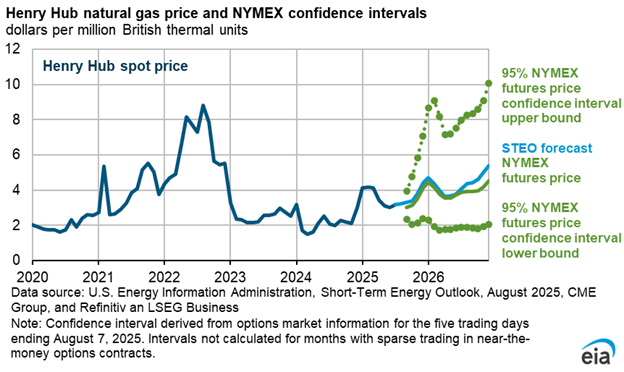

Natural Gas Outlook – Markets, Exports, and Storage

Henry Hub Price Forecast

Henry Hub Price Forecast

The forecast for Henry Hub spot prices moved lower this month, with EIA citing stronger-than-expected production and high storage levels. This outlook suggests less likelihood of extreme winter spikes, though sudden cold weather could still reverse the trend.

For industrial users and power plants, the current environment offers near-term price relief. However, decision-makers should remain cautious; the gas market has a history of sharp reversals tied to weather or unexpected outages.

LNG and Storage Dynamics

Liquefied natural gas (LNG) exports continue to climb as new terminals come online, connecting U.S. gas markets more directly to global demand. With Europe reliant on U.S. LNG and Asia’s imports growing, domestic prices are increasingly linked to overseas conditions.

At the same time, U.S. storage sits above the five-year average, which gives the system resilience. For buyers, this means a near-term buffer against shocks, but the growing role of exports means the U.S. market is less insulated than it once was.

Power Generation Mix and Renewables

Fuel Mix Shifts

Natural gas remains the largest share of U.S. generation, but renewables are rising steadily. Solar and wind continue to set records for new capacity additions, driven by falling costs and supportive policies. Coal’s decline accelerates as economics and regulations increasingly favor cleaner alternatives.

This shift affects not just emissions but also market dynamics. With variable renewable output growing, grid reliability and storage solutions are becoming more important for utilities and regulators.

Emissions Outlook

EIA projects U.S. power sector CO₂ emissions will continue to fall gradually, reflecting coal’s decline and renewables’ growth. Still, natural gas remains a cornerstone of generation, which keeps emissions reductions moderate rather than steep.

For companies with sustainability targets, this transition means cleaner grid electricity over time, but not a complete solution. Businesses may still need renewable power purchase agreements or on-site solar to hit net-zero goals.

What’s Driving These Changes?

Economic Growth and Demand Trends

Forecasts depend heavily on the health of the global economy. EIA assumes steady U.S. growth, but weakness in Europe and mixed signals from China temper demand expectations. Manufacturing activity and industrial output are especially important indicators to watch.

Policy, Weather, and Geopolitics

Federal approvals for LNG facilities, state-level renewable mandates, and international climate policy all influence supply and demand. Weather remains another major variable—unexpectedly hot summers or cold winters can quickly reshape consumption patterns.

Geopolitical risk continues to loom large. Conflicts in energy-producing regions or disruptions in global shipping lanes could create sudden shocks across oil and gas markets, making flexibility in procurement and risk management essential.

Implications for Energy Decision-Makers

Commercial & Industrial Buyers

Businesses can take advantage of the relatively soft natural gas outlook to secure favorable supply contracts or hedges. Oil price forecasts are stable but risky, meaning companies may want to diversify strategies instead of relying on a single procurement approach.

Energy efficiency investments and demand flexibility programs also gain value in volatile markets. Even when prices look calm, having the ability to shift or cut usage can protect margins during unexpected spikes.

Utilities and Power Sector

Utilities face the dual challenge of maintaining reliability while shifting toward cleaner generation. Planning for grid flexibility, investing in storage, and meeting regulatory requirements will remain key priorities.

The STEO’s continued outlook for coal’s decline and renewables’ growth reinforces that the energy transition is underway, but it also underscores the need for careful system balancing. Utilities that proactively adapt can turn these challenges into opportunities for innovation and customer value.

Conclusion – This Month’s Big Picture

The latest STEO shows an energy market that is stable in the short term but shaped by powerful long-term transitions. Oil prices remain modest but vulnerable to global risks, natural gas is abundant yet tied more closely than ever to overseas markets, and the U.S. grid continues its steady march toward renewables.

For decision-makers, the lesson is clear: don’t just track today’s numbers, but use them as a guide to adapt strategy. Flexibility in procurement, ongoing efficiency efforts, and awareness of global dynamics can make the difference between simply reacting and staying ahead.

Peoples Company is committed to providing important energy insights to help investors make smarter decisions. To learn more about our energy services, please visit us here.

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.