2022 Crystal Ball Outlook

According to the United States Department of Agriculture, Iowa has led the nation in corn production for the last 27 consecutive years and 42 of the last 43 years. In the 2021 calendar year, we witnessed spikes in market statistics for agricultural cropland in Iowa, such as $/CSR2 point, as well as a surge in both the number of auctions and in acre prices. There is no doubt the Iowa land market finished on a high note with multiple very strong indicators in 2021.

The question remains: Will these market conditions remain robust in 2022?

News regarding the increase in cropland values across the state seems to be a universal theme. Below are several sources referenced by the appraisal business line at Peoples Company:

Farm Credit Services of America published a survey on farmland throughout the Midwest. Based on this survey, cropland sales in the fourth quarter of 2021 saw an increase of 36.5% compared to the same period in 2020. The number of public land auctions through the fourth quarter were up 62% compared to 2020. Public land auctions had increased to nearly 50% of all the sales in 2021. This led to a decrease in the number of realtors, private and sealed-bid sales.

The Federal Reserve Bank of Chicago conducts an annual Agricultural Survey for “good” farmland. The most recent survey indicates that “good” farmland across Iowa increased by 10.00% from July 2021 to October 2021 and increased by 28% from October 2020 to October 2021.

Per a land survey published by the Iowa Realtors Land Institute (RLI), revised March 2021. Land values across Iowa increased by 7.8% from September 2020 to March 2021, and land values across Iowa increased by 18.8% from March 2021 to September 2021. The survey indicates a total increase of 26.6% for land value across Iowa from September 2020 to September 2021.

Iowa State University, Center for Agriculture and Rural Development, and Iowa State University Extension and Outreach publishes an annual survey every November. The 2020 survey estimates that average land values across Iowa have increased 1.7% from November 2019 to November 2020. The 2021 survey estimates a 29% increase in average land values across Iowa from November 2020 to November 2021.

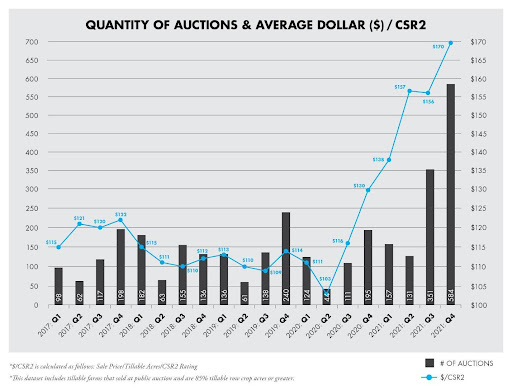

The chart below, developed by Peoples Company, illustrates these recent trends, and the data set includes farms that consist of 85%+ tillable acres that are sold through the public auction method.

The increase in auction sales and average $/CSR2 point in the 4th quarter of 2021 speaks volumes to the strength of the agricultural cropland market in Iowa at the end of 2021 and heading into 2022.

The appraisal business line at Peoples Company closely monitors high-level market statistics and market studies. These sources help describe the local market conditions and help support various adjustments and reconciliations within an appraisal report. Yet, one source of information/data that is often widely overlooked is “boots on the ground.”

Aside from in-depth research studies and analysis of numerous market transactions, information from market participants can often prove invaluable. It is good practice to develop strong relationships with property owners such as investors and owner/users, farm managers, auction houses, buyer/seller agents, and other appraisers. There is always a story behind each property that we appraise.

Most agricultural market sources report on high-level concerns such as the potential for inflation, rising input costs, rising labor costs, and potential for change in tax law to help curb the massive amount of federal stimulus spending. Other sources report on positives from the market, such as strong commodity prices, low-interest rates and strong yields.

Oftentimes, market participants might not entirely agree with some of the general market sentiments.

Three recent discussions with market participants revealed the following:

“The market is viewed as being still fairly strong, and it is important to lock in input costs/prices early to avoid volatility in the market. Try to minimize input costs by buying ahead. Many farmers made money last fall (fall 2021), and those that bought ahead are probably going to be able to weather any rough waters. Given increased input costs, it might be strategic to plant crops that demand less inputs such as soy versus corn. It might also be wise to cut back in equipment costs.”

“Now is the time to stay the course; I don’t anticipate changing my crop rotation, even with the news of potential increased input costs. Last fall, farmers generally made money, and this year should fair just the same for those that are leveraged property and have some level of scale. Those that are willing to put the work in should be able to skirt by any significant labor issues/labor shortage. Now is not the time to get irrational with spending; focus on strong yields and minimizing costs. With current trends in commodity prices, the future of agriculture is looking good.”

“It is important to remember that inflation is a very general term and likely doesn’t affect each industry and/or each portion of each industry the same way. Numerous economic factors have led the agricultural industry into somewhat of a ‘cruise control’ mentality where commodity prices are up, land values are up, lending power is strong, and the outlook for agricultural cropland is strong. Now is the time to ‘stay the course’ and maneuver each farm operation to enhance the bottom line. While commodity prices will (and always) play a large part in the demand for agricultural cropland, owners should be wary of leveraging to sustain their operations. Well leveraged and well-capitalized operations with scale should be able to weather the near-term agricultural market uncertainties.”

If you have any questions about the valuation or your land, please contact Appraisal@PeoplesCompany.com or call 855.800.5263.

Agriculture

Crop Insurance

Energy Management

Industry Insights

Land Auctions

Land Investment Expo

Land Management

Land Values

News & Events

Real Estate

Peoples Company proactively works to anticipate the needs of those in the agricultural sector. Our monthly email publication keeps readers in the know about everything land.